Brexit and Future of UK : Discussions

- Thread starter Vergennes

- Start date

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

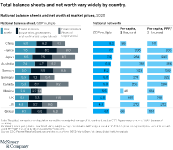

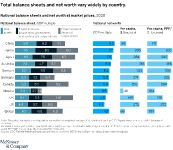

The rise and rise of the global balance sheet: How productively are we using our wealth?

Global wealth has tripled in 20 years, but how productively have we used that growth in wealth?

Attachments

Last edited:

That doesn't account for natural resources. We have oil reserves equal to 4.8x annual consumption and gas reserves equal to 2.6x. Total value $1.2tr.The net worth of the UK, taking into account its debts, is £10.7 trillion in 2020, which is €12.20 trillion, while France's net worth, also taking into account its debts, is €18.97 trillion. This explains the very advantageous conditions we have when we borrow.

United Kingdom Oil Reserves, Production and Consumption Statistics - Worldometer

Current and historical Reserves, Production, and Consumption of Oil in the United Kingdom. Global rank and share of world's total. Data, Statistics and Charts.

United Kingdom Natural Gas Reserves, Production and Consumption Statistics - Worldometer

Current and historical Reserves, Production, and Consumption of Natural Gas in the United Kingdom. Global rank and share of world's total. Data, Statistics and Charts.

UK natural capital accounts - Office for National Statistics

Estimates of the financial and societal value of natural resources to people in the UK.

www.ons.gov.uk

The chart above also seems very dubious. E.g.:

1. Why is the value of German non-financial corporations half what France's is (GDP multiple or not)? That doesn't make even the slightest bit of sense to anyone reading, unless French companies are massively, massively overvalued.

2. Why is France's GDP so low compared to the values of its companies? Sounds again like France's companies are massively overvalued.

On per capita $, we are fairly close anyway and our companies are clearly more productive and less overvalued due to higher per capita GDP.

Last edited:

What use is value if it can't pay the debt? It's only worth as much as the GDP per year, because that's what you raise revenue off and that's what pays the debt interest. Seems to be both a meaningless and questionable stat.

What it tells me is that German companies are massively undervalued and French companies are massively overvalued. If I was an investor having seen this, I would sell all my French stocks and buy German, Australian and Mexican non-financial stocks to get better returns.

What it tells me is that German companies are massively undervalued and French companies are massively overvalued. If I was an investor having seen this, I would sell all my French stocks and buy German, Australian and Mexican non-financial stocks to get better returns.

Last edited:

WAIT one second. German values in multiples of GDP are 5.3, 4.2 and 5.4, yet the overall multiple is 6.0????

Equally, UK values are 5.1, 5.3 and 11.5 but overall multiple is 4.8.

This chart is meaningless unless somebody can provide the full maths behind it and a breakdown of the figures for each country.

Equally, UK values are 5.1, 5.3 and 11.5 but overall multiple is 4.8.

This chart is meaningless unless somebody can provide the full maths behind it and a breakdown of the figures for each country.

WAIT one second. German values in multiples of GDP are 5.3, 4.2 and 5.4, yet the overall multiple is 6.0????

Equally, UK values are 5.1, 5.3 and 11.5 but overall multiple is 4.8.

This chart is meaningless unless somebody can provide the full maths behind it and a breakdown of the figures for each country.

Because German industrial asset alone is worth a trillion pound which is may be little more than England's.

Nominal GDP is divided by this deflator, yielding real GDP. Nominal GDP is usually higher than real GDP because inflation is typically a positive number.

Industrial asset would fall under 'asset of non-financial corporation'.Because German industrial asset alone is worth a trillion pound which is may be little more than England's.

Nominal GDP is divided by this deflator, yielding real GDP. Nominal GDP is usually higher than real GDP because inflation is typically a positive number.

You're talking about PPP vs nominal, I understand that bit, but it doesn't explain the inconsistencies mentioned. And debts are not paid in PPP $s.

So let me explain a little:

As far as natural resources are concerned, this is well taken into account:

It's in AN.2 non-produced non-financial, item AN.21 Natural resources, AN212 Mineral and energy reserves.

As far as GDP multipliers are concerned, each component of the value is a multiple of GDP and therefore the total value is the sum of the three, for Germany for example the values are 5.3; 4.2; and 5.4 which makes a total value of 14.9. But then you have to subtract the financial liabilities and this total reduces to 6.

For the value of our companies it is because we own a lot of companies, or shares of companies abroad, it is a consequence of our history, by the way the UK too.

And per capita UK 195/218 and France 296/355, I think it's quite different.

As far as natural resources are concerned, this is well taken into account:

It's in AN.2 non-produced non-financial, item AN.21 Natural resources, AN212 Mineral and energy reserves.

As far as GDP multipliers are concerned, each component of the value is a multiple of GDP and therefore the total value is the sum of the three, for Germany for example the values are 5.3; 4.2; and 5.4 which makes a total value of 14.9. But then you have to subtract the financial liabilities and this total reduces to 6.

For the value of our companies it is because we own a lot of companies, or shares of companies abroad, it is a consequence of our history, by the way the UK too.

And per capita UK 195/218 and France 296/355, I think it's quite different.

Please list these liabilities.So let me explain a little:

As far as natural resources are concerned, this is well taken into account:

It's in AN.2 non-produced non-financial, item AN.21 Natural resources, AN212 Mineral and energy reserves.

As far as GDP multipliers are concerned, each component of the value is a multiple of GDP and therefore the total value is the sum of the three, for Germany for example the values are 5.3; 4.2; and 5.4 which makes a total value of 14.9. But then you have to subtract the financial liabilities and this total reduces to 6.

For the value of our companies it is because we own a lot of companies, or shares of companies abroad, it is a consequence of our history, by the way the UK too.

And per capita UK 195/218 and France 296/355, I think it's quite different.

Stocks overseas are included in NIIP and you are worse than us for that.

Net international investment position - Wikipedia

Seems to me that your assets are overvalued, particularly property.

Yep, you've had twice the increase in real estate stock relative to GDP.

"Nearly all net worth growth from 2000 to 2020 occurred in the household sector as a result of growing equity and real estate valuations"

199% vs 111%

At the end of the day, only revenue on GDP pays for debt, and you are worse than us on that score. The rest is just based on highly questionable valuations (i.e. estimates), not real data.

Yep, you've had twice the increase in real estate stock relative to GDP.

"Nearly all net worth growth from 2000 to 2020 occurred in the household sector as a result of growing equity and real estate valuations"

199% vs 111%

At the end of the day, only revenue on GDP pays for debt, and you are worse than us on that score. The rest is just based on highly questionable valuations (i.e. estimates), not real data.

Please list these liabilities.

| Monetary gold and special drawing rights (SDRs) |

| Currency and deposits |

| Debt securities |

| Loans |

| Equity and investment fund shares |

| Listed shares |

| Insurance, pension and standardised guarantee schemes |

| Financial derivatives and employee stock options |

| Other accounts receivable/payable |

You know, McKinsey&Company is not French !!Seems to me that your assets are overvalued, particularly property.

Yep, you've had twice the increase in real estate stock relative to GDP.

"Nearly all net worth growth from 2000 to 2020 occurred in the household sector as a result of growing equity and real estate valuations"

199% vs 111%

At the end of the day, only revenue on GDP pays for debt, and you are worse than us on that score. The rest is just based on highly questionable valuations (i.e. estimates), not real data.

Please list the values and how they're counted.

Monetary gold and special drawing rights (SDRs) Currency and deposits Debt securities Loans Equity and investment fund shares Listed shares Insurance, pension and standardised guarantee schemes Financial derivatives and employee stock options Other accounts receivable/payable

Doesn't affect what I said.You know, McKinsey&Company is not French !!

1. Your real estate is inflated.

2. You can't pay off debt with questionable theoretical evaluations of non-liquid assets.

3. How they count assets and liabilities for banks is weird anyway.

Basically it's a bunch of BS. In terms of what actually matters - GDP and National Debt and Tax Revenue - France is doing worse than the UK.

All that really matters:

France

Debt - EUR 2916bn

Tax Revenue - EUR 570bn - (19.5% with higher taxes than UK)

France General Government Debt

Government Debt in France increased to 3536.10 EUR Billion in the first quarter of 2026 from 3460.50 EUR Billion in the fourth quarter of 2025. This page provides the latest reported value for - France General Government Debt - plus previous releases, historical high and low, short-term forecast...

tradingeconomics.com

tradingeconomics.com

France - Tax Revenue (current LCU) - 2026 Data 2027 Forecast 1972-2023 Historical

Tax revenue (current LCU) in France was reported at 652280000000 LCU in 2023, according to the World Bank collection of development indicators, compiled from officially recognized sources. France - Tax revenue (current LCU) - actual values, historical data, forecasts and projections were sourced...

tradingeconomics.com

UK

Debt - £2450bn

Tax Revenue - £522bn (21.3% - and with lower tax rates than France!)

United Kingdom Public Sector Net Debt Ex Banks

Government Debt in the United Kingdom increased to 2984.30 GBP Billion in May from 2940.80 GBP Billion in April of 2026. This page provides the latest reported value for - United Kingdom Public Sector Net Borrowing - plus previous releases, historical high and low, short-term forecast and...

tradingeconomics.com

United Kingdom - Tax Revenue (current LCU) - 2026 Data 2027 Forecast 1972-2023 Historical

Tax revenue (current LCU) in United Kingdom was reported at 743081000000 LCU in 2023, according to the World Bank collection of development indicators, compiled from officially recognized sources. United Kingdom - Tax revenue (current LCU) - actual values, historical data, forecasts and...

tradingeconomics.com

Last edited:

Look at it this way. A house might with worth £500k on paper but if the owner doesn't keep up mortgage payments and the bank needs to foreclose it at an auction, you ain't getting £500k for it. Likely you only get half of that. And if your real estate is overvalued anyway because its gone up twice as much as everyone else's, well.... Couple that to the dubious valuation of French corporations relative to more productive German ones and I wouldn't place much stock in this report at all.BMD better than McKinsey&Company to evaluate countries' net worth !

And you know how to take this into account better than McKinsey&Company? It's just an excuse to justify your biases.Look at it this way. A house might with worth £500k on paper but if the owner doesn't keep up mortgage payments and the bank needs to foreclose it at an auction, you ain't getting £500k for it. Likely you only get half of that. And if your real estate is overvalued anyway because its gone up twice as much as everyone else's, well.... Couple that to the dubious valuation of French corporations relative to more productive German ones and I wouldn't place much stock in this report at all.

Fact. You can't pay debts with the hypothetical valuations of non-liquid assets. And French companies being valued higher than German ones, despite only half the productivity does not make sense to anyone. If value is so high, why is productivity so low and debt so high?And you know how to take this into account better than McKinsey&Company? It's just an excuse to justify your biases.